A company's inventory cost accounting method can have a direct impact on its primary financial statements - balance sheet, income statement, and statement of cash flows. Businesses can employ one of two inventory accounting procedures under the US generally accepted accounting standards (GAAP) that are first-in, first-out (FIFO), or last-in, first-out (LIFO) inventory valuation methods. Do you know about it? Let’s study the LIFO-FIFO Inventory Cost methods and then check their formulas and examples in this article.

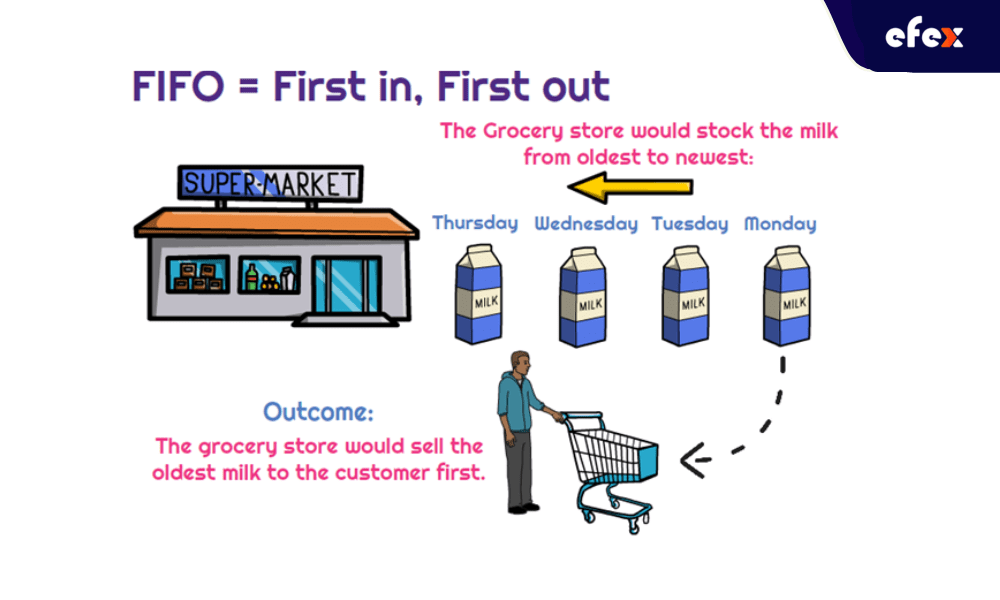

FIFO stands for first-in, first-out and it's used to estimate cost flows. The mechanism of shifting the cost of a company's product from its inventory to its cost of goods sold is referred to as cost flow assumptions. The term "inventory" describes:

The FIFO approach is based on the presumption that a company's oldest units have been sold first. As a result, the corporation will use those exact inventory costs when calculating COGS (cost of goods sold). Although the oldest inventory may not always be the first to sell, the FIFO approach is only concerned with inventory totals and not with physical inventory. However, for the COGS calculation to function, FIFO makes this assumption.

- See more: Order Management System: Definition, Process, And Value

- See more: Order management system for eCommerce: Definition, Key Effect, Benefit

Determine the price of your oldest inventory to compute COGS (Cost of Goods Sold) using the FIFO method. Multiply the cost by the number of inventory sold. The term "inventory sold" refers to the cost of items purchased for resale or the cost of goods created (which includes labor, material & manufacturing overhead costs).

Keep in mind that a company's inventory pricing is subject to change. These varying expenses must be factored into the equation.

For example, if a corporation sold 100 units of an item, 75 units were purchased at $10.00 and 25 units were acquired at $15.00, the company cannot apply the $10.00 cost price to every unit sold. Only 75 pieces are available. The remaining 25 products must be allocated to the higher, $15.00, pricing.

Finally, the product must have been sold to be included in the calculation. Unsold inventory cannot be factored into the cost of goods calculation.

The FIFO method is more reliable than the LIFO ("Last-In, First-Out") method in my opinion. The following are some of the benefits of using the FIFO technique:

Because the disparity between expenses and profits is bigger using the FIFO approach, a corporation may have to pay more income tax (than with LIFO). The FIFO technique must also be used with caution so that profit is not overstated. This can happen when the product cost grows and that of goods estimate is based on the newer numbers rather than the actual cost.

👉 Read More: Excess Inventory: Definition, Disadvantages And How To Reduce

The following is how the FIFO approach calculates inventory cost: Assume a product is produced in three batches over a year. Each batch's costs and quantities are as follows:

=> The total number of pieces produced was 7,100. The total cost came to $28,600. The average cost of one piece is $4.03. The unit costs for each batch generated must then be calculated.

Let's say you sold 6,000 units out of a total of 7,100 during the year. You have no idea which pieces were sold for what price. Under FIFO accounting, you begin by assuming that you have sold the oldest (first-in) produced stock first to establish the cost of units sold.

So, considering FIFO, of the 6,000 units sold: You presume that the first 3,000 Batch 1 goods, each valued at $4, were all sold. The first 3,000 units from Batch 1 sold for $4.00 each. A total of $12,000 has been spent. The next 2,500 pieces from Batch 2 sold for $3.6 each, totaling $9,000. And the final 500 units from Batch 3 sold for $4.75 a piece, totaling $2,375.

The overall cost of the 6,000 goods sold is $23,375 when these costs are added together.

👉 Read More: Just-in-time Inventory (JIT): How It Works And Its Advantages

Note: This computation is inaccurate since it is impossible to establish which items from which batch were sold in which order in this type of situation. It's just a method of obtaining a calculation.

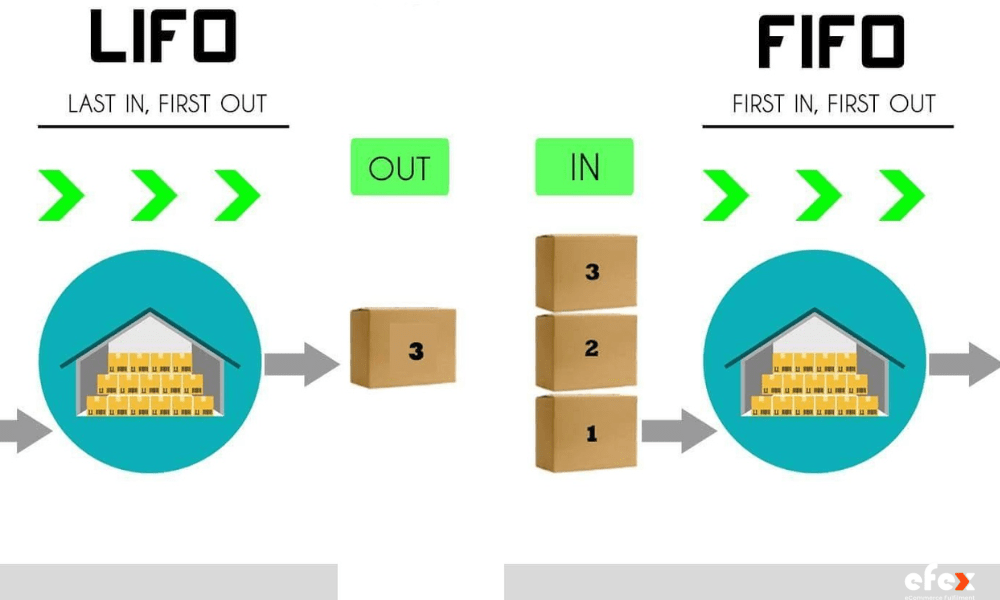

LIFO is the inventory valuation method that is the polar opposite of FIFO, in which the most recent item purchased or acquired is the first item out. When compared to FIFO, this results in deflated net income expenses and lower inventory ending balances in inflationary environments.

The average cost inventory approach charges the same price for each item. The average cost method is calculated by dividing the cost of products in inventory by the total number of items offered for sale. As a result, net income and closing inventory balances differ between FIFO and LIFO.

Finally, when all components traceable to a final product are known, specific inventory tracing is used. If all of the parts are unknown, any method other than FIFO, LIFO, or average cost is applicable.

LIFO is an acronym that stands for "Last-In, First-Out." LIFO is the inverse of FIFO, supposing that the most recent products added to a company's inventory are sold first. The expenses of inventory will be used in the COGS (Cost of Goods Sold) calculation. When the cost of inventory is rising owing to inflation, the LIFO approach of financial accounting may be preferred over FIFO.

Because the more expensive products in inventory are sold off first when using the FIFO inventory valuation method, the cost of a sale will be higher.

👉 Read More: Real-Time Inventory Management: How It Works And Benefits

Furthermore, because a corporation would make less profit, the taxes it will pay will be lower. These savings might add up over time to be significant for a firm. Only in the United States is the LIFO approach authorized.

Determine the cost of your most current inventory to use the LIFO method to compute COGS (Cost of Goods Sold). Multiply it by the number of stock sold. If the cost of acquiring inventory products fluctuates throughout the period for which you are computing COGS, you must account for it, just as you would with FIFO.

LIFO costing ("last-in, first-out") considers the most recently created things to be the most recently sold. In this situation, you would expect Batch 3 items to be sold first, followed by Batch 2 items, and finally the remaining 800 items from Batch 1. Under the LIFO approach, the total cost of 7100 inventory sold would be $19,800. LIFO results in a higher cost of goods sold and a lower closing inventory.

The cost of goods sold will be lower under FIFO, while the closing inventory will be larger. In times of dropping prices, however, the opposite will be true.

A corporation can utilize either the inventory valuation FIFO ("First-In, First-Out") or LIFO ("Last-In, First-Out") method when calculating the cost of goods sold in the United States. Although both are legal, the LIFO method is commonly criticized since bookkeeping is substantially more difficult and the mechanism is easy to manipulate. Corporate taxes are lower because the LIFO method allows a business to spend its most recent product expenses first.

👉 Read More: Cost Of Lost Sales: Formula And How To Solve

Historically, these prices have risen over time. Profit reductions may provide tax benefits, but they may also make a business less enticing to investors. Because it is a simple method for assessing the cost of products sold, FIFO is popular among investors and financial institutions.

It's also more straightforward for management to keep track of finances because of its simplicity. Many companies, particularly those in the United States, have made FIFO a policy.

Now you have had some basic knowledge of the LIFO-FIFO Inventory Cost Method via the above information. Hope this article provides you with useful information to apply to your inventory control effectively. Don't forget to follow Efex via our Fanpage or website to read more interesting articles! Thank you for reading! See you in the next post!