More Helpful Content

Inventory refers to all of the final materials or items utilized in manufacturing that a firm owns. Once sold, these things are expensed as COGS (cost of goods sold) on the income statement, an essential indicator used to analyze profits and assess how effectively a firm manages labor and materials in the manufacturing process. Businesses have numerous ways to estimate which expenses are taken from inventory and reported as COGS. The inventory cost flow assumptions are one of them. Let’s dive into it in this article to understand more.

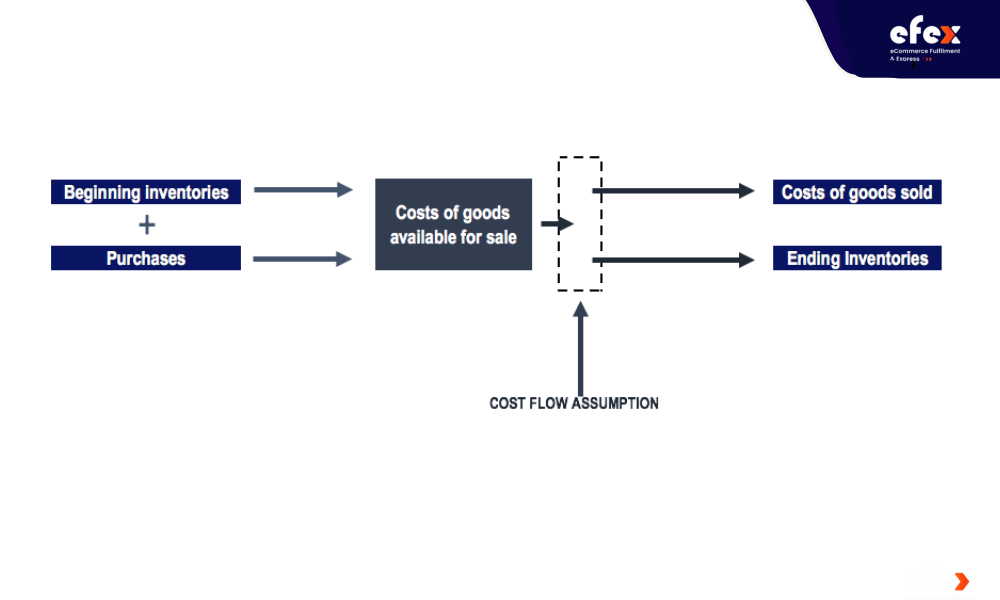

The inventory cost flow assumption refers to the cost of an inventory item that fluctuates once it is manufactured or purchased and sold. Management needs a formal method for allocating costs to inventory since it transitions to sellable commodities due to the cost disparity. The phrase cost flow assumption relates to the process of removing expenses from a business’s inventory and reporting them as the cost of goods sold.

Cost flow assumptions in the United States contain FIFO (first in, first out), LIFO (last in, first out), and average. It is not necessary to assume if explicit identification is used. FIFO, LIFO, and average are assumptions since the flow of expenses out of the inventory do not have to reflect how the goods were physically removed from inventory.

Let’s assume your company spends $50 on a gadget on March 1. You continually purchase a similar gadget for $100 on July 1 and then another identical gadget for $150 on October 1.

The goods can be used interchangeably. Your company sells one of the gadgets on December 1. You paid three distinct prices for the gadgets. Thus, what cost should you declare for the cost of the goods sold? The cost flow assumption can be interpreted in a variety of ways.

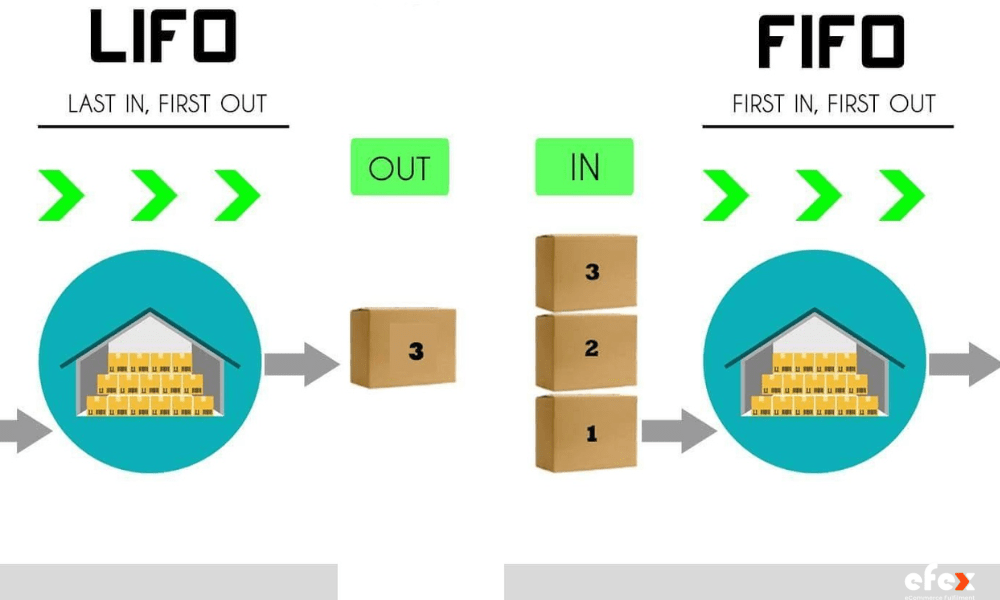

According to the (first in, first out) FIFO system, the first thing bought is also the first thing sold. As a result, the cost of the product sold would be $50. Profits would be higher under FIFO because this is the cheapest gadget in the scenario.

As the latest-in, first-out strategy, it that the most recent item acquired is also the most recent thing sold. As a result, the cost of goods sold would be $150. Because this is the most expensive item in the above scenario, earnings would be the lowest under LIFO.

You may physically determine which exact products are bought and then sold using the specific identification technique, and therefore cost flow changes with the real item sold. It is an unusual circumstance because most products are not uniquely recognizable.

The weighted average technique, or the average cost flow assumption, calculates the goods sold cost as the average of all three units, which is $100 based on the above example. This cost flow assumption technique will likely provide a mid-range cost and a mid-range profit.

The inventory cost flow assumption may not always correspond to the real movement of products. Businesses prefer to use an assumption of cost flow to reduce profits and maximize earnings to increase share value. Companies often choose one of 2 strategies to allocate expenses across different manufacturing stages, which are FIFO( first in, first out) and LIFO. While the FIFO (first in, first out) technique presupposes that the first item added to inventory is the first to be sold, the LIFO strategy assumes that the last products to come into goods are sold first.

The FIFO (first in, first out) technique is favorable in periods of rising prices since the expenses reported are low and the income is larger. On the other hand, the LIFO approach is commonly used when tax rates are increased since the costs allocated are greater, and the revenue is lower. If inventory costs are largely consistent over time, the products sold cost will not fluctuate much regardless of whether the cost flow assumption is applied.

In contrast, significant changes in inventory costs over time will result in a discrepancy in reported profit rates based on the cost flow assumption utilized. Therefore, the accountants should be particularly aware of the financial implications of the inventory cost flow assumption in variable cost periods.

However, you should note that the LIFO technique is not permitted under IFRS. If more accounting systems take this attitude in the future, the LIFO (last in, first out) technique may no longer be accessible like a cost flow assumption.

Another substitute is using the weighted average approach. All prior difficulties become less important. This technique tends to produce average profitability and average rates of taxable revenue throughout time.

Some advantages and disadvantages come with the average cost flow assumption technique. One of its biggest benefits is that the average cost flow assumption removes the necessity to track every object, which can be useful when high numbers of comparable commodities pass through inventories. This strategy involves less effort, is far less expensive to implement than other inventory cost methods, and is less likely to alter income theoretically.

However, there are certain disadvantages that you should consider. The average cost flow assumption presumes that all units are equal, which is not necessary. For example, newer batches of the same commodities or material may be marginally superior to earlier ones, thus attracting a higher price.

If you use a just-in-time inventory management system or transact your whole inventory in a particular accounting period, your cost flow assumption is irrelevant. Because all your inventory costs will be converted to COGS by the end of the quarter, your choice of cost flow assumption has no impact on your company’s financials. On the other hand, companies that keep inventory for an extended period should select a cost flow assumption that meets their needs.

Because of its simplicity, the weighted average cost technique is better suited for enterprises that do not utilize accounting software to maintain inventory or sell merely a few types of items. However, most small businesses use the LIFO (last in, first out) approach to save cost on taxes, which results in increased operating cash flow for your company.

We can not deny that inventory cost flow assumptions play an important role in inventory management. Hopefully, you can improve not only your inventory management but also your business operation, resulting in a significant increase in your business's revenue via the knowledge of this article. You've found this article so helpful? Do not forget to follow our Fanpage and come back to our homepage to read many interesting articles!