More Helpful Content

Since calculating work in process inventory is a time-consuming procedure that includes connecting a cost with a percentage of completion, understanding it is critical for calculating and managing inventory and production capacity. To do that, you should first learn about what it is so that you can apply it to your inventory management in practice.

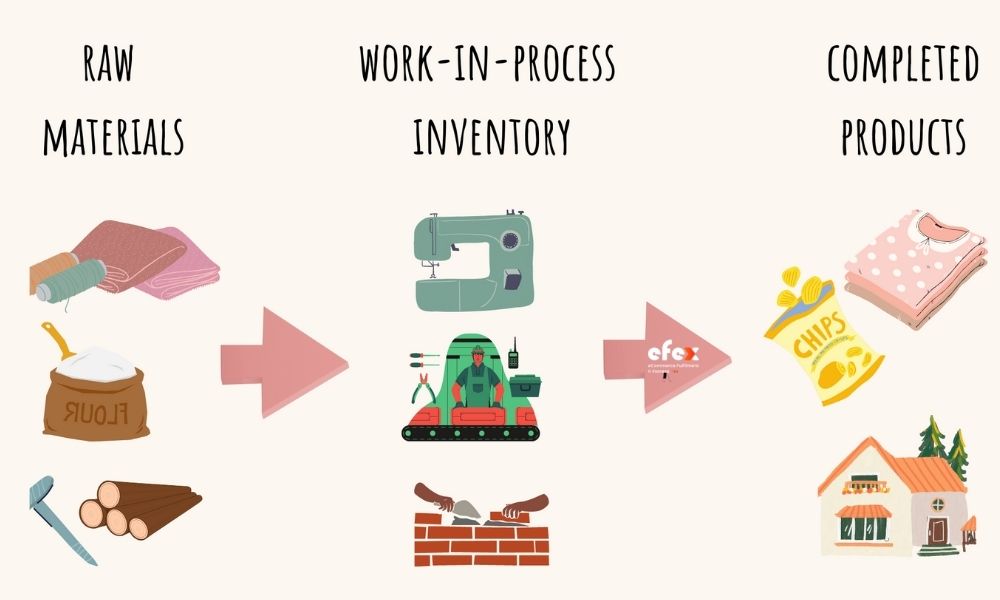

Work In Process (WIP) Inventory is a kind of inventory that has been partly finished during the production process. These products are usually kept in the manufacturing area, although they might alternatively be kept to one side in a buffer storage facility. Because raw materials are frequently introduced at the start of the conversion process, the cost of work-in-process generally includes all raw material costs related to the end product. It also has another name called work-in-progress, which both abbreviated as WIP inventory. Although they have the same meaning, there are still specific differences, which we will discuss in the latter part.

The process for calculating the cost of WIP inventory is quite complicated. Before attempting to assess their worth, you must grasp the following phrases connected to WIP inventory.

The cost of the assets in the preceding accounting part of the balance sheet is the beginning work-in-process inventory cost. To determine its cost, you must first identify the value at its beginning period and carry it forward as an asset in the fiscal year.

The manufacturing cost is the cost incurred when producing a final product. Overhead, labor, and raw materials costs are all included in this cost. The greater the usage of WIP inventory in the production process, the higher the value of raw materials and labor. This does not affect the overall cost of manufactured items.

Manufacturing Cost = Raw Material + Labor Cost + Overhead Cost

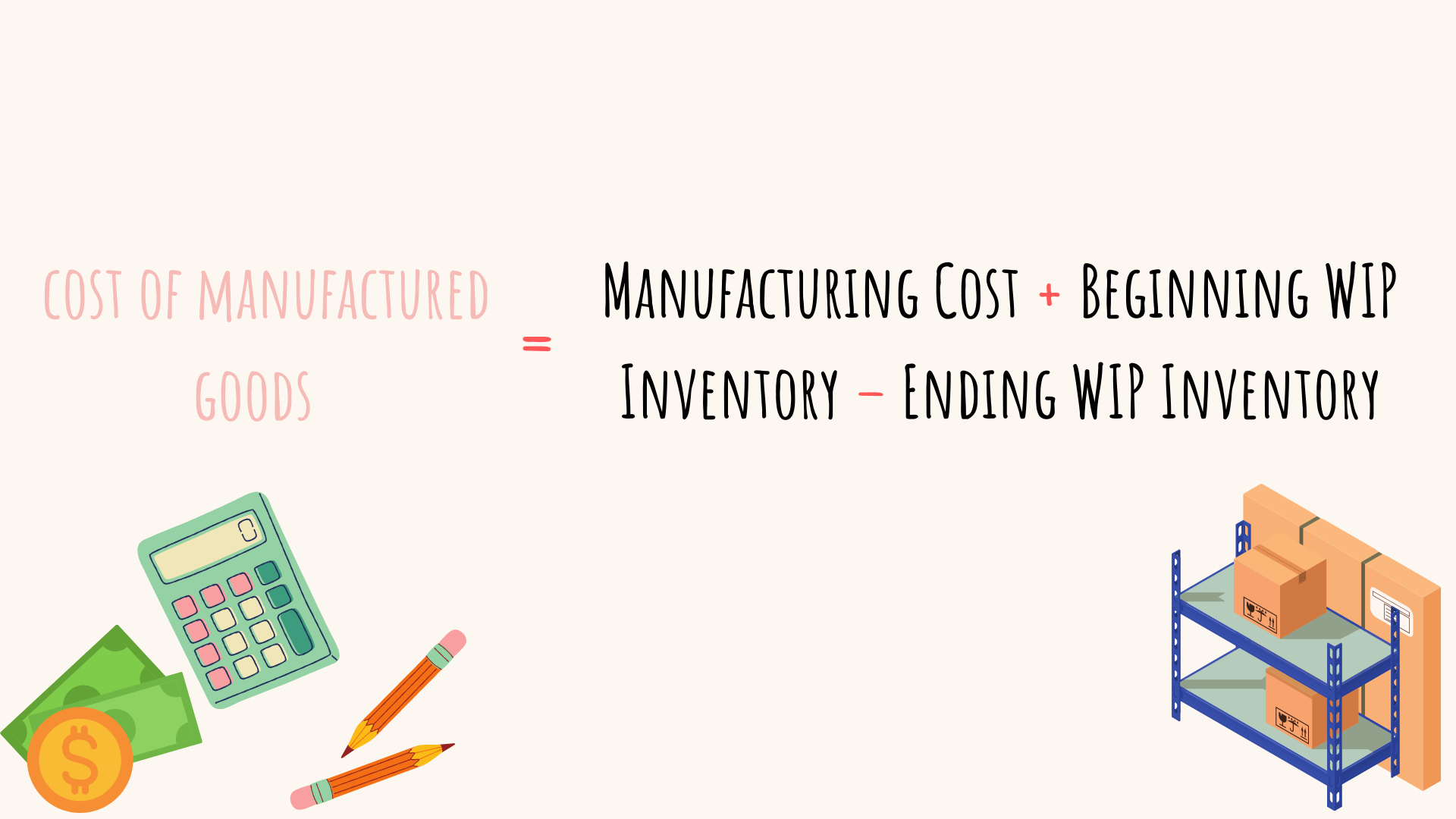

As discussed earlier, the cost of manufacturing comprises the costs of raw materials, overhead, and labor. It is the cost of producing the finished product. The cost of manufactured goods must compute the value of WIP inventory.

Cost Of Manufactured Goods = Manufacturing Cost + Beginning WIP Inventory - Ending WIP Inventory

These two words are mostly interchangeable. Both terms are abbreviated as WIP inventory. As defined, work-in-process inventories are commodities that are only partially completed. These items are also known as goods-in-process. Some people define it as items that go from raw ingredients to final products in a short amount of time. While the term "work-in-progress" is usually used to describe activities that take a long time to complete, building projects are an example. This distinction may not be the standard. Therefore, wither phrase can be used to refer to incomplete things in most cases.

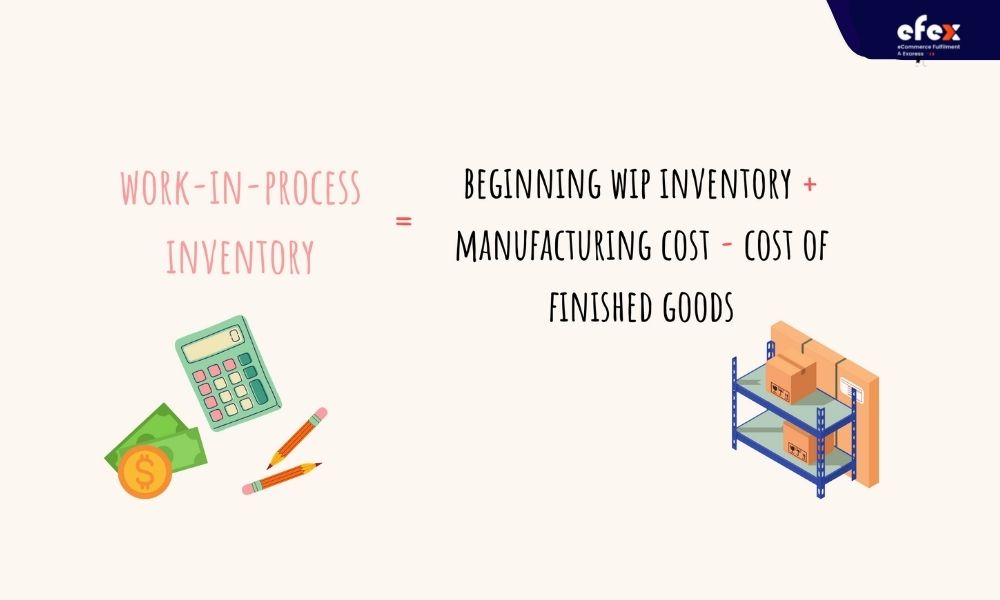

Work-In-Process Inventory = Beginning WIP Inventory + Manufacturing Cost - Cost Of Finished Goods

Work-In-Process Inventory = Beginning WIP Inventory + Manufacturing Cost - Cost Of Finished Goods

The total work-in-process inventory value is the sum of the ending WIP for one accounting period and the beginning for the next. On a balance sheet, this ending inventory quantity is shown as a current asset.

👉 Read More: Is Inventory A Current Asset: Definition and Example

To do that, you must first determine the initial work-in-process inventory and then determine the final one.

The WIP inventory is known as the raw materials as well as labor and manufacturing costs for the large majority of enterprises. More complicated processes, such as large building projects, may involve labor, subcontractor charges, and other expenses. That is the reason why many manufacturers decrease this inventory before totaling it after the accounting time.

The beginning WIP inventory and the ending one is the same, except for a specific accounting period. WIP inventory is always calculated after accounting times, no matter they are quarters, years, or other periods. This total amount represents the conclusion of the accounting period’s work-in-process inventory and the start of the following accounting period. On your company’s current balance sheet, this ending WIP inventory is recorded as a current purchase. Therefore, to find out the way to identify it, you must first understand what it means. So you will need the finishing WIP value to do that.

The ending WIP is calculated by the following formula:

Ending WIP Inventory = Beginning WIP Inventory + Manufacturing Costs - Cost Of Finished Goods

Assume Yellow Mushroom Shop holds a $10,000 initial work-in-process inventory for the 3 months. This includes all of the fresh mushrooms, bags, labels, and additional raw ingredients that are waiting to be transformed into completed bags or mushrooms available to buy. The company will spend $75,000 over the next three months processing and wrapping mushrooms. Three months later, the finished items’ total value will be $72,000. Yellow Mushroom Shop currently has $13,000 in inventory that is not raw materials or finished goods. Growing WIP inventory levels for a consumable product like mushroom are not a good sign unless they are appropriately stored as anticipation inventory.

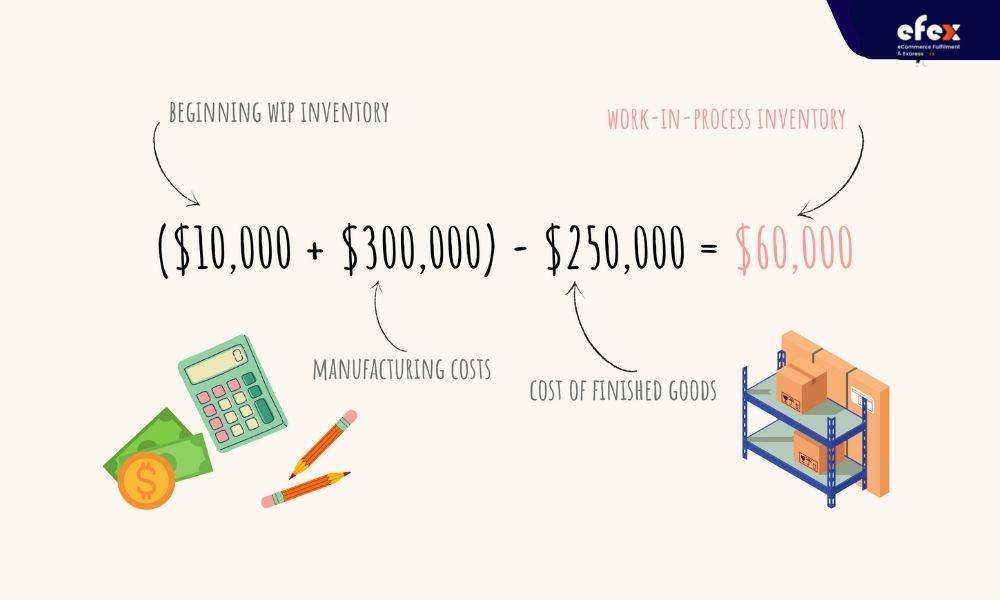

Assume you buy $10,000 of raw material at the beginning of the year. You spend $300,000 on production and generate completed items for $250,000. The work-in-process number implies that your business has $60,000 in inventory that is neither finished goods nor raw material, but your work-in-process inventory.

Tracking this kind of this inventory necessitates some accounting. You might be wondering how a WIP inventory journal entry appears if you are not an accountant. For example, the first time you buy $5,000 in raw material that is deducted from the raw materials inventory. The identical amount would then be credited to your invoices payable. When the raw materials are in the manufacturing cycle, that $7,000 debit will be transferred to the WIP inventory account, and then the raw materials account is credited with $7,000. Finally, after the inventory is converted to completed products, $7,000 is deducted from the finished goods account and it will be credited back to the work-in-process inventory account.

👉 Read More: Journal Entry For Obsolete Inventory: Example And Calculation

👉 Read More: Perpetual Inventory System Journal Entry: Example, Calculation

👉 Read More: Manufacturing Overhead Journal Entry

As you can see high work-in-process inventory intensity is not a good thing and is commonly disregarded. However, keeping track of this parameter has significant advantages.

As it is an inventory asset, failing to get it on your company’s balance sheet might lead to an undervaluation of overall inventory. Consequently, your completed items will be overpriced. It is essential to maintain it for tax purposes to have an exact analysis of what your inventory is valuable.

Managers should be concerned about rising work-in-process inventory levels. A high goods-in-process inventory quantity might suggest that your production process is not running properly and bottlenecks may exist. By measuring it, you may identify and eradicate problems before they harm your bottom line.

Some businesses count their work-in-process inventory physically to calculate the value depending on the present state of each unit in the production process. This consumes a significant amount of time and diverts your staff's attention away from skilled activities. This time, you will need to use the above WIP formula to estimate accurately the worth of your inventory.

Three things you should keep in mind when you have too much work in process inventory are fewer storage spaces for the most profitable products, more capital for unsaleable items, and higher risks of becoming obsolete goods and incomplete goods expiring.