More Helpful Content

To estimate demand and avoid surplus stock, all companies must keep track of how much inventory they own. Therefore, every manufacturing company uses the inventory record system to maintain track of its inventory movements throughout the year. Inventory systems are classified into two types: periodic and perpetual.

Each system has different advantages, so if you are in charge of selecting and implementing an inventory system for your organization, it is critical to grasp the distinctions between the two of them.

However, many businesses are confused by these two techniques, that is why this article is published to help you differentiate the differences between the periodic and perpetual inventory systems.

Inventory refers to any raw resources and completed commodities that businesses keep on hand for manufacturing or that are sold to customers on the market. Periodic inventory and perpetual inventory are the two forms of inventory. Both of them are accounting systems used by organizations to keep track of the number of things they have on hand. Nevertheless, they are fundamentally distinct.

While periodic inventory requires a physical count at different points in time, perpetual inventory is automated and uses point-of-sale and enterprise asset management systems. The first one is less expensive to accomplish, but the second one requires more time and money.

👉 Read More: What Is Centralized Inventory? Benefit And Drawback

👉 Read More: What Is In-Transit Inventory? Example And Formula

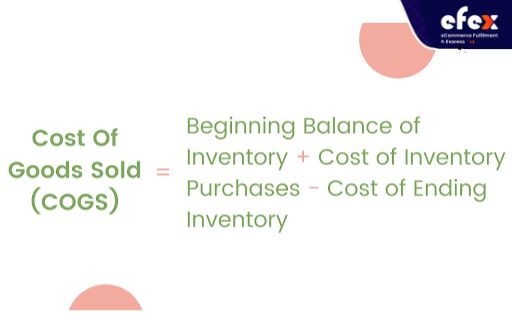

Smaller firms that have less inventory or do not have a huge amount of money or the ability to adopt automated systems into their workflow frequently employ the periodic inventory system. As a result, they conduct periodic physical counts to determine their inventory and the cost of products sold which is known as COGS. The cost of goods sold is a critical accounting indicator that reflects a business’s gross margin when reduced from revenue.

Cost Of Goods Sold (COGS) = Beginning Balance Of Inventory + Cost Of Inventory Purchases - Cost Of Inventory Purchases - Cost Of Ending Inventory

Businesses may not be conscious of how much inventory they have unless they do frequent inventory counts such as weekly, monthly, or yearly. The procedure is as follows:

Because firms sometimes carry numerous goods, completing a physical count may be hard and time-consuming. Consider running an office supply business and attempting to count and track every ballpoint pen on the shelf. Multiplying it by the number of items in an office supply chain.

This is why many businesses only do a physical count once every quarter or even every year. This implies that the inventory account and COGS data for organizations using a periodic method are not always extremely updated or precise.

The perpetual inventory system is an inventory control approach in which every inflow and outflow of merchandise is continually updated using an electronic point-of-sale system. The records kept by this system are constantly up-to-date.

In this method, an inventory ledger is kept to preserve a thorough and continuous record of inventory transactions and issues, with the closing balance being the inventory in hand. The following is how the closing inventory is calculated:

Inventory At The End = Inventory At The Beginning + Receipts - Issues

Perpetual inventory is a complex mechanism. Inventory changes are accurate as long as no things are stolen or damaged and may be retrieved quickly. The cost of goods sold account is also regularly updated as each transaction is made. The data captured digitally is relayed in real-time to the central databases.

Since it includes the technology, it necessitates relatively little work from enterprises:

Due to the costs involved in installing and maintaining the infrastructure, this sort of inventory system can be highly expensive. The system is significantly easier to use than the periodic system. It provides not only real-time tracking, but is also far more precise than physical counts.

Furthermore, because each product has a barcode, businesses may obtain more complete data on everything that enters and exits their facilities.

👉 Read More: What Is Inventory Allocation? Methods And Benefits

The periodic inventory and perpetual inventory systems are two ways of tracking the number of products on hand. The perpetual system is the most advanced of the two, but it takes considerably more records management to maintain. The periodic method depends on an infrequent physical stock count to calculate the final inventory balance and cost of products sold, whereas the perpetual system will keep track of inventory balances continuously.

This table provides the general differences between these two inventory systems.

| Comparison factors | Periodic Inventory System | Perpetual Inventory System |

| Meaning | Track every single detail of inventory as it occurs | Record technique in which inventory records are updated regularly |

| Basis | Book Records | Physical Verification |

| Updations | Continuously | When the accounting period ends |

| Information | Inventory and cost of sales | Inventory and cost of goods sold |

| Balancing Figure | Inventory | Cost of goods sold |

| Possibility Of Inventory Control | Yes | No |

| Affect On Businesses Operation | No | Yes |

The comparison table of the periodic inventory system and the perpetual inventory system

The primary distinction between periodic and perpetual accounting is time. Periodic inventory is performed after a period in order to generate financial statements, while perpetual is created as a result of sales and inventory acquisitions.

Here are the key distinctions between these two systems that you should know.

It clearly shows that the perpetual inventory system outperforms the periodic inventory system. The primary situation in which a periodic system can sound right is when the quantity of inventory is extremely modest and can be visually reviewed without the require for more thorough inventory records.

Because warehouse personnel may mistakenly record inventory transactions inaccurately in a perpetual system, the periodic approach can also operate effectively when they are inadequately taught in the usage of the perpetual inventory system.

👉 Read More: What Is Perishable Inventory? Example And Model

- Read More: Order Management System: Definition, Process And Value

- Read More: Order Management System For Ecommerce: Definition, Key Effect, Benefit

Through the comparison of the periodic and perpetual inventory systems above, you can see that the periodic inventory system is much less expensive than the perpetual inventory system, but it provides more accurate data for continuing inventory tracking and quick confirmation.

Furthermore, the income reports are created promptly since the inventory records are correctly preserved in the perpetual inventory system, which is not feasible in the periodic system.

Finally, the perpetual inventory system is ideal for large firms with complicated inventory levels and higher sales volume, such as grocery businesses and pharmacies, whereas the periodic inventory system is suitable for small companies. Hope you have a good time with Efex.