More Helpful Content

ABC analysis in inventory management is one of the most popular inventory management techniques. Depending on the value of items, the ABC analysis divides it into three categories A, B, and C. Companies can better prioritize their inventory, streamline processes, and make informed decisions by classifying their inventory using ABC analysis. Going ahead, we'll go through what is ABC analysis of inventory, explain how to apply it, and assist you in determining whether it's appropriate for your company.

ABC analysis refers to a technique of managing inventory that figures out the value of inventory products based on their worth to the company. Inventory managers classify products according to how ABC prioritizes them based on demand, pricing, and risk.

Some businesses could choose a classification scheme that divides goods into more than just those three categories. The ABC analysis of inventory management is distinct from the ABC analysis used for costing systems, also known as activity-based costing. Activity-based costing is a manufacturing technique used by accountants to allocate overhead or indirect expenses, such as wages or utility costs, to goods and services.

- Read More: Order Management System: Definition, Process And Value

- Read More: Order management system for Ecommerce: Definition, Key Effect, Benefit

According to the Pareto Principle, only 20% of efforts or causes result in 80% of the outcomes in every system. ABC analysis for inventory control determines the 20% of commodities that provide around 80% of the value in accordance with Pareto's 80/20 rule. As a result, the majority of companies have a small quantity of A items, a somewhat bigger group of B items, as well as a large group of C items, which is the category that describes the vast majority of products.

| Type | Importance | Percentage of Total Inventory | Yearly Consumption Value | Controls | Records |

| Class A | High value | 10% – 20% | 70% – 80% | Tight | High Accuracy |

| Class B | Medium value | 30% | 15% – 20% | Medium | Good |

| Class C | Low value | 50% | 5% | Basic | Minimal |

It's possible that the Pareto Principle isn't always correct. Analysis, nevertheless, reveals that valued goods do lean toward an 80/20 distribution. The use of Pareto's Principle to rank and prioritize particular inventories over others is one way it contributes to ABC analysis in inventory management. By organizing all of your goods into three categories, ABC analysis simplifies inventory analysis and allows you to create more tactical decisions.

By dividing the cost of an item by the yearly revenue of that item, do an ABC inventory analysis. The findings help you prioritize your use of human and financial resources by letting you know which products are most important and which provide the lowest profits. For an ABC inventory analysis, you can use this calculation:

Besides, you can perform a fundamental ABC inventory analysis using Microsoft Excel. List each good or service in decreasing order of the value of its product utilization.

Imagine that you manage an online store selling women's accessories. You've just had a successful season, and now you can finally examine your inventory. As you can see from the table below, your most popular things are earrings and shoes, but neither of those items is expensive, therefore they don't bring in a lot of money. Although you just sold 13 designer purses, they nevertheless account for 70% of your sales. It is obvious that purses belong in group A, shoes in group B, and earrings in group C. What will you do with such an analysis at this point? In order to enhance sales, you may start by investing more effort in locating the greatest designer purses. You might also spend a lot of money promoting your choice of purses or negotiating favorable terms with suppliers. You can wish to add more things to your inventory so that your consumers have more options.

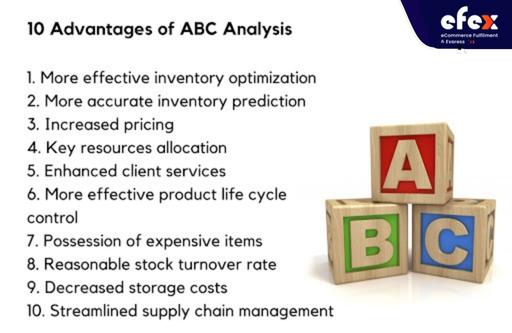

Inventory ABC analysis improves capital investment cost management. The information gathered from the research lowers outdated stock and can increase inventory turnover rate, and how frequently a company has to buy new inventory after running out of old stock.

Employing ABC analysis to manage inventory will provide a wide range of advantages, including

The study pinpoints the goods that are popular. The business can use its limited warehouse space to maintain reduced inventory levels for Class B and C items while sufficiently stocking those products.

- Read More: ABC Analysis Example, Formula, and How To Calculate

- Read More: What is return merchandise authorization (RMA) And Process

Accurate sales forecasting may be improved by tracking and gathering data on items with significant consumer demand. In order to raise the company's total revenue, managers can utilize this data to define inventory levels as well as pricing.

A spike in sales for a particular product indicates that demand is rising and that a price rise may be appropriate, increasing profits. Informed vendor negotiation. Class A products account for between 70 and 80 percent of a company's revenue, therefore it makes sense to bargain for favorable terms with suppliers. Try to negotiate post-purchase services, minimize payment discounts, free delivery, or any other cost savings if the provider won't agree to decrease prices.

To make sure that Class A goods are in accordance with customer needs, resource allocation is regularly assessed using ABC analysis. Reclassify the goods as demand declines to effectively use staff, resources, and facilities for the new Class A items.

Numerous variables, including sales volume, item price, as well as profit margins, affect service levels. Offer better levels of service for such things that you've found to be the most profitable.

Understanding a product's life cycle stage—launch, development, maturing, or decline—is essential for projecting demand and properly stocking inventory levels.

The success of a business is highly correlated with class A inventory. Make it a priority to keep an eye on demand and to maintain good stock levels so that it is always sufficient essential products available.

Through systematic inventory management and data gathering, keep the stock turnover rate at desirable levels.

You can cut the expenses associated with maintaining extra inventory by carrying the proper percentage of stock depending on A, B, or C categories.

To lower carrying expenses and streamline operations, do an ABC analysis of available data to decide whether it's time to switch to a specific source or combine suppliers.

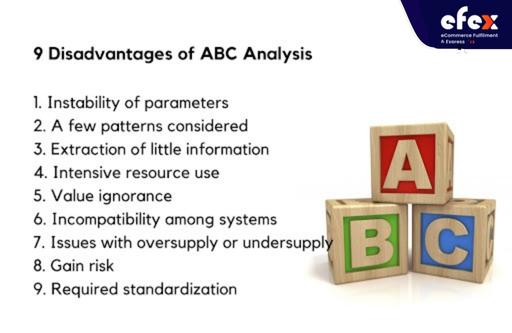

Given all of its advantages for managing inventory and its maintenance, ABC analysis is not a unique inventory management system. The usage of an ABC analysis is impacted by the unique consumer demands trend, categories, and systems, as well as other problems that each firm encounters. The focus on the financial status of inventory and the considerable amount of time and personal discipline to use the approach are two drawbacks of ABC analysis. Here are some more difficulties:

Managers frequently allocate up to 50% of products to a new class quarterly or yearly as an outcome of ABC analysis. Since organizations sometimes don't become aware of what's happening until there is a demand issue, the necessity to reassess might waste time and harm customer happiness.

Aspects like new product releases or market seasonality won't be taken into consideration by the conventional ABC technique. For instance, the lack of a prior customer base may explain a new product's poor sales volume. When demand is changing or uncertain, ABC analysis will produce inventory problems since it provides a rather static view of demand.

The statistical information or level of detail required to develop smart management decisions may not be fully covered by ABC class information.

Bikeshedding is the practice of giving excessive weight to unimportant topics, which is a regrettable outcome of ABC analysis. Staff members may add their ideas or seek their own variations because ABC analysis is simple to understand, turning it into a resource-intensive process instead of a time-saving solution.

According to ABC analysis, product relevance is determined by revenue or usage frequency, yet some products could defy this paradigm. A product display retail could, for instance, sell very little yet draw a lot of consumers thanks to its novelty. In the aerospace industry, a certain component for a plane could not be utilized frequently and have low market value, yet it might provide a crucial safety role.

The ABC inventory analysis does not adhere to widely accepted accounting rules (GAAP) and is in disagreement with conventional costing methodologies. Running numerous costing systems will increase labor expenses and inefficiencies.

There is a chance of running out of Class B or C products since the ABC analysis looks at monetary values instead of the quantity that moves through inventories. The opposite can also take place. If you repeatedly order low-class things without reviewing them, you can end up with excesses that build up in your inventory.

Class B and C products nevertheless have worth even if their value is lower than that of Class A goods. The fact that surplus stocks are constantly at risk of deterioration or damage is among the ABC analysis's shortcomings. As a result, merchandise that is routinely unmonitored or uncounted might be stolen.

The uniformity of materials, which includes how they are identified, kept, regularly graded, and monitored, is necessary for the ABC technique to be effective on every item.

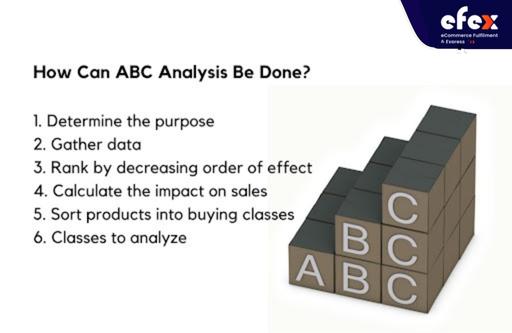

The first step in a complete ABC analysis is to determine the goal you're aiming towards. After you have it, gather the data you'll need to classify the products. Following the implementation of the classes, continuously monitor the information and base choices thereon. Here are the steps for doing an ABC analysis:

Determine the purpose. By managing inventory levels of the appropriate goods based on client sales or production, an ABC analysis can help you achieve one of two goals: decrease procurement costs or increase cash flow.

Gather data. The annual expenditure for each item is the most typical type of data to gather. Raw purchase dollars are used for this data. You may gather information on the weighted cost, including gross profit margin, ordering, and carrying costs if the calculation is simple.

Rank by decreasing order of effect. Using the ABC analysis technique, rank the cost of every inventory item in decreasing order of effect, starting with the most expensive.

Calculate the impact on sales. For every inventory item, get the percentage effect on sales by dividing the yearly item cost by the total cost of all products purchased. When comparing items on the list, you will utilize this percentage or fraction. Here is the equation: % Effect= (Annual item cost / Aggregated total of all items purchased) x 100

Sort products into buying classes. After you've established the classes, focus on contract negotiations, supplier consolidation, changing the sourcing approach, or introducing e-procurement. Making adjustments in these areas can result in considerable cost savings or guarantee the availability of Class A products in stock. Instead of being rigid about the rule 80/20, adopt a comprehensive view.

Classes to analyze. Once categories and a proactive cost management plan have been established, schedule evaluations to check on the final outcome of selections.

Applying ABC analysis consistently and reviewing it frequently yields the greatest results. The following are some best practices to follow while doing ABC analysis in your company:

It is essential to keep your ABC analysis categories straightforward to simplify your inventory management. Your teams should have no trouble identifying which goods fall under a particular category right away. For instance, popular categorization techniques include using the product's cost or frequency of sales.

A labor level, or the number of hours spent working on a certain inventory class, should be allocated to each categorization. Generally, higher labor levels should be assigned to a classification if it has a greater value or influence on the company.

Each categorization should be evaluated in accordance with the guidelines established by the original ABC analysis. This entails a unique set of KPIs, performance evaluations, and a strategy for reordering or offloading any excess inventory.

The original ABC study considered several product categories and the current state of the company. It's crucial to review the current categories and, if required, reclassify when inventories and markets shift. Think about changes in sales by product and class, emerging business rivals, and consumer trends.

Tracking any changes in product turnover and sales may be done with the use of inventory software. You can simply utilize an inventory management system to automatically track and provide reports to identify any significant areas that need improvement if you have a set of rules and procedures in place.

The technique of counting certain goods from your inventory on predetermined dates is known as a cycle count. Some businesses utilize cycle counting to generate monthly count lists for different parts of their warehouse. However, depending on how frequently stock levels change, the frequency may change. Cycle counting can be customized with ABC analysis, which improves the inventory management system for your particular requirements. For instance, you can determine that while B products only have to be recorded once every three months, your A products must be counted monthly. As you only measure inventory that is classified by class when ABC analysis is used for cycle counting, you will save a lot of time and effort. If not, you are confined to counting every individual object at the same intervals.

The easiest strategy to adopt ABC inventory management is to determine if it will work for your company first. By raising detailed questions, prevent making assumptions. Make all the following essential preparations for a better execution as soon as you decide to go forward.

- Read more: Tracking Signal Formula And Example

A company will effectively assess the value of its goods by using an ABC analysis for inventory management. Large volumes of inventory can be managed with the support of this straightforward method, which also determines how many resources should be given to each categorization in order to maximize profits. After all, you should think about utilizing specialized software that can further streamline the inventory management procedure. Hope you have a good time with Efex.