More Helpful Content

Overhead costs are recurring expenses associated with running a company. Accountants divide manufacturing company operating expenses into two categories: fixed manufacturing overhead and variable manufacturing costs. These expenses are used by managers in a number of ways.

For example, an executive team must first assess a company’s production overhead expenses in order to undertake a profitability analysis and establish the price at which their products must be sold to generate a profit. The fixed overhead costs of businesses vary greatly based on the nature of the organization and the way management defines fixed costs.

In this article, we are going to go through about the fixed manufacturing overhead definition, its calculation, and specific examples about it.

Fixed manufacturing overhead is a collection of costs that never change as a result of fluctuates. These expenses are required to run a business. The complete amount of fixed overhead expenses that a firm incurs should constantly be known so that managers can make plans to generate enough margin from the product and service sales to at least meet the balance of fixed overhead. If not, making a profit is difficult and impossible.

👉 Read More: Manufacturing Overhead Budget: Example And Formula

Fixed overhead expenditures include the following:

Because fixed overhead expenses do not vary significantly, they are straightforward to estimate and should seldom deviate from the planned amount. These expenses also seldom fluctuate from one period to the next, except if a change is induced by a contract adjustment that changes the cost.

For instance, facility rent remains constant until a planned rent rise changes it. Instead, a fixed asset’s recognized depreciation may lower the amount of impairment expenditure related to that asset.

When assessing fixed production overhead, there are two variances that are computed and assessed, including fixed overhead spending variance and fixed overhead volume variance.

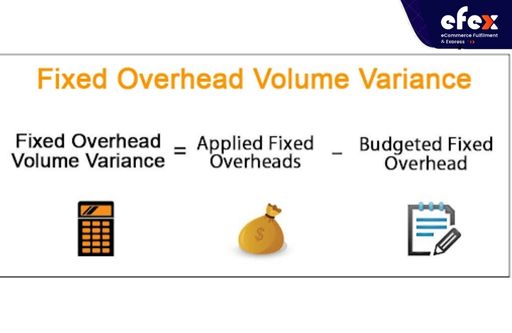

The discrepancy between actual and estimated fixed overhead expenditures is referred to as the fixed overhead spending variance, whereas the discrepancy between planned and actual fixed overhead expenses is the fixed manufacturing overhead volume variation.

Business cannot ascribe any part of this difference to the effective or ineffective utilization of employees since fixed overhead expenses are not normally driven by activities. In reality, fixed overhead has no effectiveness variance.

Now, let’s move to the fixed overhead volume variance.

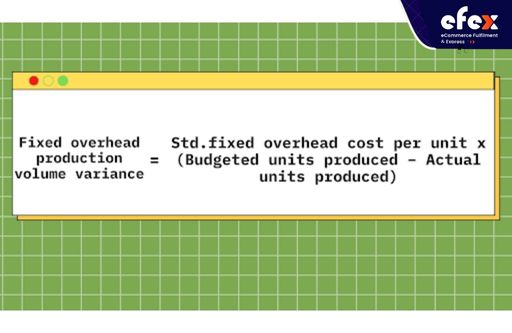

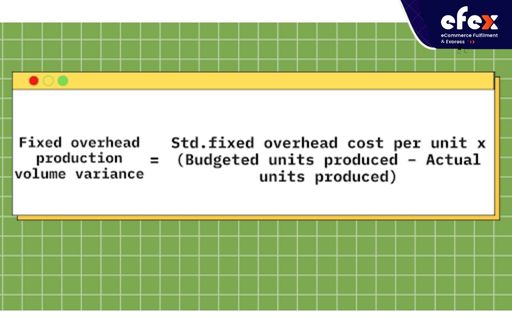

However, before delving into the it, keep in mind that the fixed overhead manufacturing volume variation should not be confused with the variable overhead effectiveness variance. The fixed overhead volume variation is mainly due to the difference between budgeted and actual output.

It is a direct outcome of the volume or units differential between budgeted and actual output. All other variables, like standard direct work hours per unit and standard wage per direct labor hour, are maintained constant. We then have the following formula:

Since the corporation manufactured and sold more units than expected, the fixed overhead volume variation is beneficial.

Assume firm ABC pays $10,000 per month for a work office in a building. This is known as a fixed overhead expense that must be met. Furthermore, the building’s property taxes would be a constant cost because they do not vary with volume sales. Fixed overhead expenditures are normally steady and cannot deviate from the planned levels for such costs.

But, if a firm’s sales exceed what it anticipated, fixed overhead expenses may rise when employees are recruited and additional managers and administrative personnel are employed.

Furthermore, if a building must be enlarged or a new manufacturing facility must be rented to match rising sales, fixed overhead expenses must rise to keep the firm functioning efficiently.

👉 Read More: What Is Manufacturing Overhead? Formula And Example

👉 Read More: Manufacturing Overhead Journal Entry: Definition & Process

The following processes are used to assign fixed overhead expenses to products:

Fixed overhead expenses may vary if activity levels vary significantly outside of their regular range. For instance, if a firm wants to expand its current manufacturing facility to accommodate a significant rise in demand, this would lead to a higher rent expenditure, which is generally considered as a part of fixed overhead.

As a result, fixed overhead expenses do not fluctuate within just a company’s regular range of operation, but they might vary beyond that range. A step cost happens when this type of shift occurs.

👉 Read More: Order Management System: Definition, Process And Value

👉 Read More: Order Management System For Ecommerce: Definition, Key Effect, Benefit

Since the fixed manufacturing overhead plays an important role in companies, it is necessary to understand this overhead cost, which can help company owners to know their expenditures in order to efficiently control their spending. Greater sales and manufacturing volumes, on average, result in higher total costs. However, because certain expenses are fixed, the percentage rise in total costs is smaller than the percentage rise in revenue and manufacture.