More Helpful Content

There are numerous techniques for inventory valuation, but WAC (or weighted average cost) is one of the most crucial techniques. This is one of the inventory control techniques that most businesses employ in inventory operations to determine the cost of inventory. This article will provide you with all the information you require concerning the weighted average perpetual inventory system.

As the name implies, the perpetual inventory method of inventory accounting involves tracking the inventory "perpetually" when it flows through the supply chain. With this method, warehouse managers continuously monitor inventory balances, meaning that if a product is acquired or sold across a point of sale, the inventory is automatically updated.

👉 Read More: Lifo Perpetual Inventory Method: Formula And Example

👉 Read More: Fifo Perpetual Inventory Method: Formula And Example

The Weighted Average Cost (or WAC) refers to the average cost of products sold for the existing inventory. For a perpetual inventory system, the WAC is calculated in a different method. Every time a transaction or purchase occurs in WAC, a standard average selling price is assigned to every inventory item. Because with a perpetual inventory system, items change under real-time circumstances, the calculation that takes a certain period into account cannot be discovered. WAC is typically used to compute an average unit price, finishing inventory, and COGS for a period of time.

Under a perpetual and periodic inventory system, the weighted average cost technique produces various allocations of inventory costs. The business performs a finishing inventory count and uses product costs to calculate the ending inventory cost in a periodic inventory system. The COGS can then be calculated by adding the initial and ending inventory costs, as well as the purchases made during the time. Inventory levels and COGS are continuously tracked via a perpetual inventory system. For the control of inventory levels, the perpetual inventory system offers more up-to-date information. This kind of inventory tracking, though, can be expensive for a business. The weighted average cost approach is also known as "moving average cost method" in a perpetual inventory system. In the sections that follow, we'll apply the weighted average cost approach to show how the allocation of inventory expenses differs in a perpetual inventory system with an example.

A business reported a starting inventory of 300 units. The unit cost is $100 at the start of the January 1 financial year. The following purchases were made by the company during the first quarter:

The following sales were also made by the business:

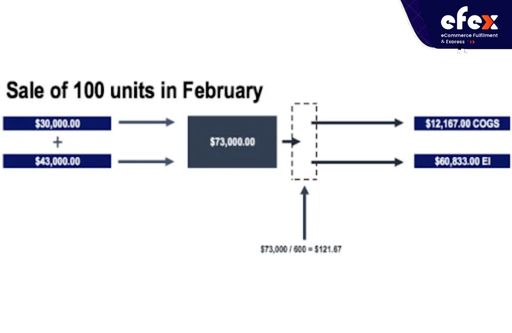

Prior to unit sales, we would calculate the average under the perpetual inventory system. So, prior to the February sale of 100 units, WAC would be:

WAC per unit = ($30,000+$13,000+$30,000)/600=$121.67

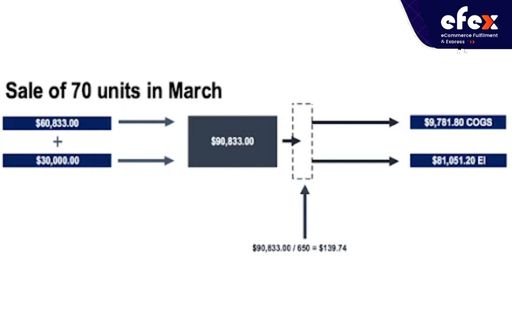

The expenses for the selling of 100 units in February would be set out as follows: COGS: $121.67x100 = $12,167 $60,833 remaining inventory = $73,000 – $12,167 Prior to the March sale of 70 units, WAC would be: WAC per unit = ($60,833+$30,000)/650=$139.74

The expenses for the selling of 70 units in March would be set out as follows: COGS: $139.74x70 = $9,781.80 $81,051.20 in finishing inventory = $90,833 – $9,781.0

We could see that the expenses are distributed varied based on whether it is a perpetual or periodic inventory system by comparing the value assigned to inventory and COGS.

In a periodic inventory system, calculations using the average cost technique are performed at the conclusion of the accounting period, with the weighted average cost based on the price of the initial inventory and all items purchased during a certain period. The units sold as well as the units kept in inventory are then calculated using this average cost per unit. The overall cost of the products that are ready to be sold is averaged when using the average cost approach, and any two pieces are offered at the average price. In fact, a sale could happen at the start of a period prior to completed purchases there at the conclusion of the same period can be disregarded by a company with the periodic inventory system. The average cost calculation is used to determine the WAC per unit, which is just the sum of the initial inventory and acquisitions.

Unlike the periodic approach, the perpetual inventory system constantly records transactions, and whenever a transaction occurs within the accounting period, average cost method calculations are made. The price of the initial inventory and all purchases made up until the moment of a sale are used to calculate the WAC per unit. Under a weighted average perpetual inventory system, sales or purchases are handled chronologically, and each time a sale is performed, a WAC per unit computation is required.

👉 Read More: Perpetual Inventory System Calculator: All Formula

👉 Read More: Periodic Inventory System Calculator: All Formula

Have you already got everything needed when it comes to the weighted average perpetual inventory system? If you do, we hope you find this post useful for you! Thank you! Hope you have a good time with Efex.